At the 2025 Indonesia Mining Conference & Critical Metals Conference - Coal Industry Conference, hosted by SMM Information & Technology Co., Ltd. (SMM), supported by the Indonesian Ministry of Foreign Affairs as a government supporter, and co-organized by the Association of Indonesian Nickel Miners (APNI), the Jakarta Futures Exchange, and China Coal Resource, Vasudev Pamnani, Director of I-Energy Natural Resources, analyzed the Indian coal market situation (special topic on the Asian market).

01 Background of India's Coal Industry

India's coal mining history dates back over 250 years, originating in the eastern region.

• India holds 378.21 billion tons of coal reserves, making it one of the world's largest coal reserve holders.

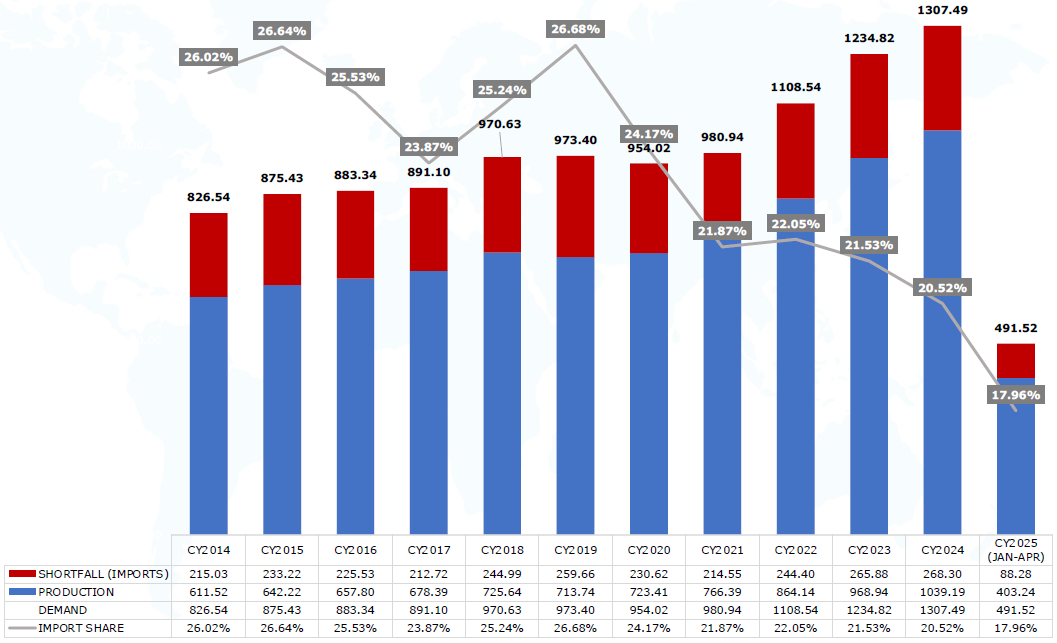

• In 2024, India ranked second globally in coal consumption (1.3 billion tons), production (1.04 billion tons), and imports (268 million tons).

• In the first four months of 2025, this momentum was largely maintained, with coal consumption reaching 492 million tons.

• Domestic coal production during the same period reached 403 million tons, a 3% increase compared to the same period last year.

• In contrast, import trends weakened, dropping to 88 million tons from January to April 2025, a 5% decrease from 93 million tons in the same period last year.

• The main challenges facing India's coal imports are increased domestic production and supply, high inventories at power plants, mines, and ports, as well as the adverse impacts of weak global demand and global trade tensions.

• The international market is also under pressure, with coal demand cooling in early 2025 due to macroeconomic instability.

• Despite coal prices falling to multi-year lows, demand remained sluggish during India's summer peak electricity usage period.

• The market remains fragile, but this does not signal the end of India's coal era.

• Coal remains the backbone of India's power sector and will continue to be an important part of the country's energy framework in 2025.

02 India's Coal Demand

Total Coal Demand in India (in million tons)

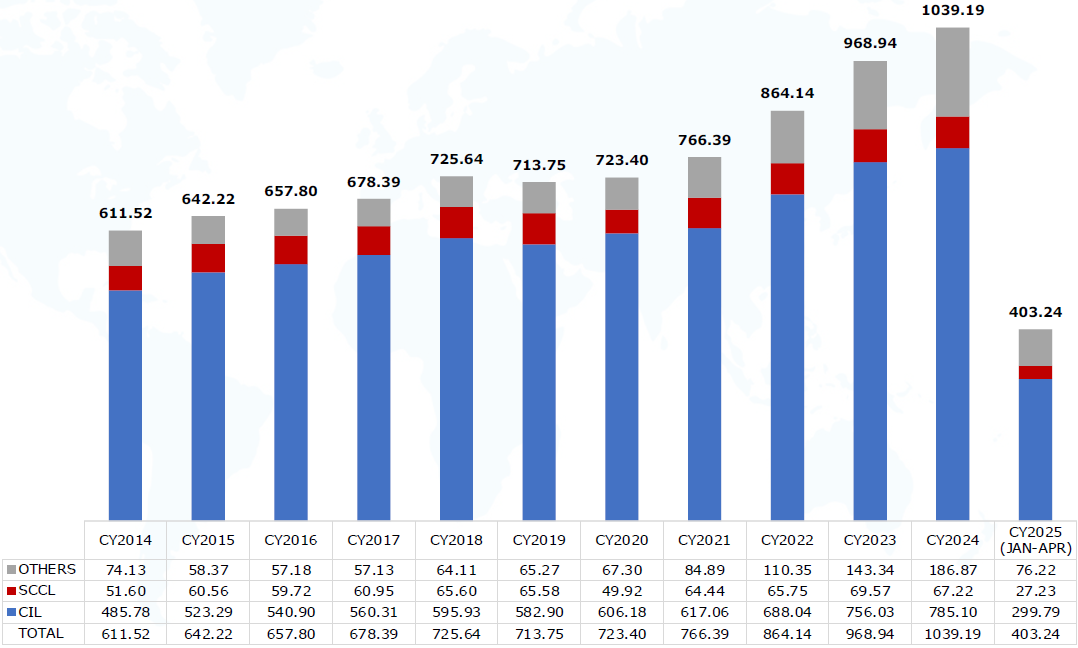

03 Domestic Coal Production in India

Coal Production in India (in million tons)

In addition, he also elaborated on perspectives such as coal dispatched from India to industries, drivers of coal demand in India, and "Black Diamond: Coal Supports India's Power System."

System Support: Indian Government Support for the Coal Industry

• Commercial Mining

• Auction Allocation System

• Revenue Sharing Model

• One-Stop Approval

• Sustainable Development and Technology

• Infrastructure Investment

• Exploration and Technology Development

• Coalbed Methane (CBM)

• E-Auction by Coal India Limited (CIL)

• Coking Coal Mission

• Coal Gasification and Liquefaction

• Reopening Closed Mines

• Coal Washing Plants

• Allowing 100% Foreign Direct Investment

• Mine Closure and Reclamation

04 Overview of India's Coal Imports

Key Factors and Insights: Why India Imports Coal

Geographical Distribution: Coal is concentrated in the central-south and eastern regions, with other areas relying on imports;

Inland Logistics and Infrastructure Challenges: High costs hinder domestic coal transportation;

Low-Grade Domestic Coal Forces India to Rely on High-Grade Coal Imports;

Government Priorities: Concentrated investment in the power sector leads to other industries relying on imports;

Import-Based Coal Power Plants: Customized power plants designed to burn imported coal;

Coking Coal Challenges: Unsuitable for steel production processes, necessitating diversification.

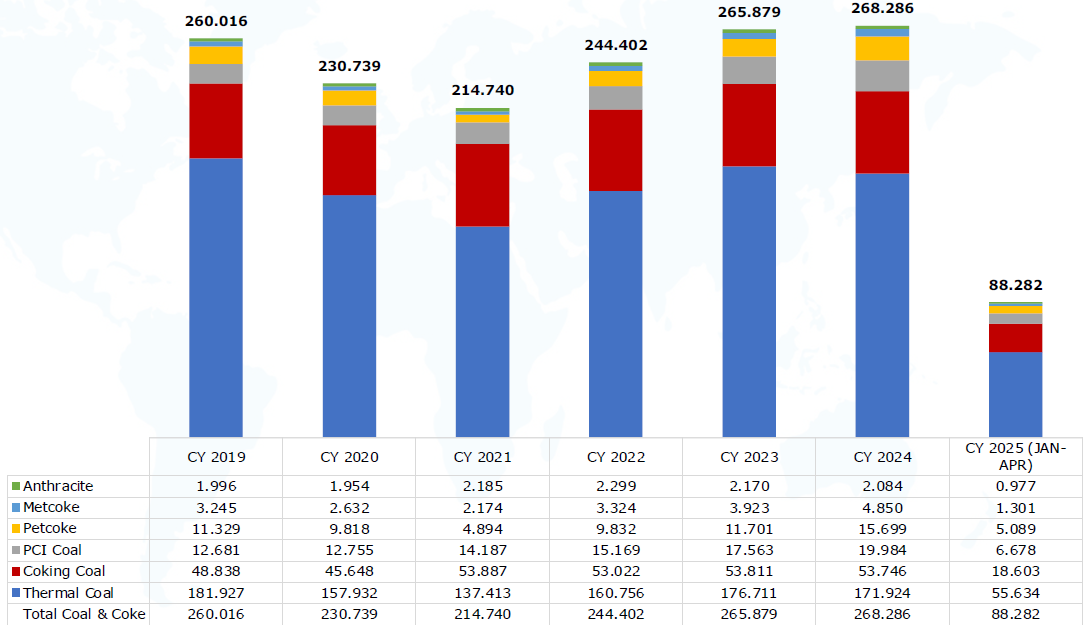

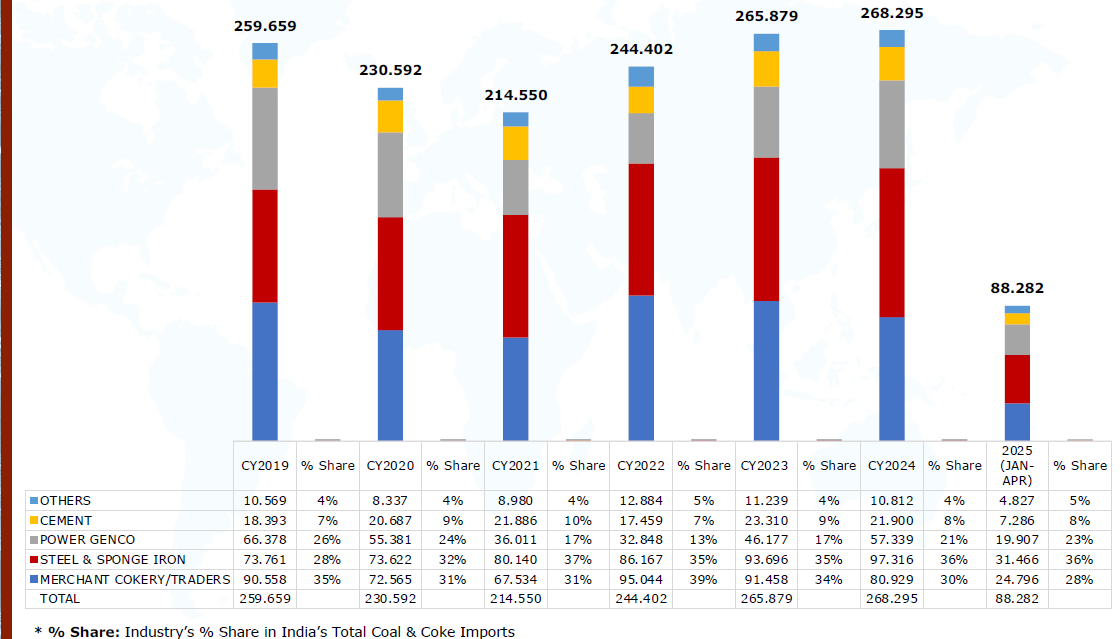

Total Coal and Coke Imports to India (1 million mt)

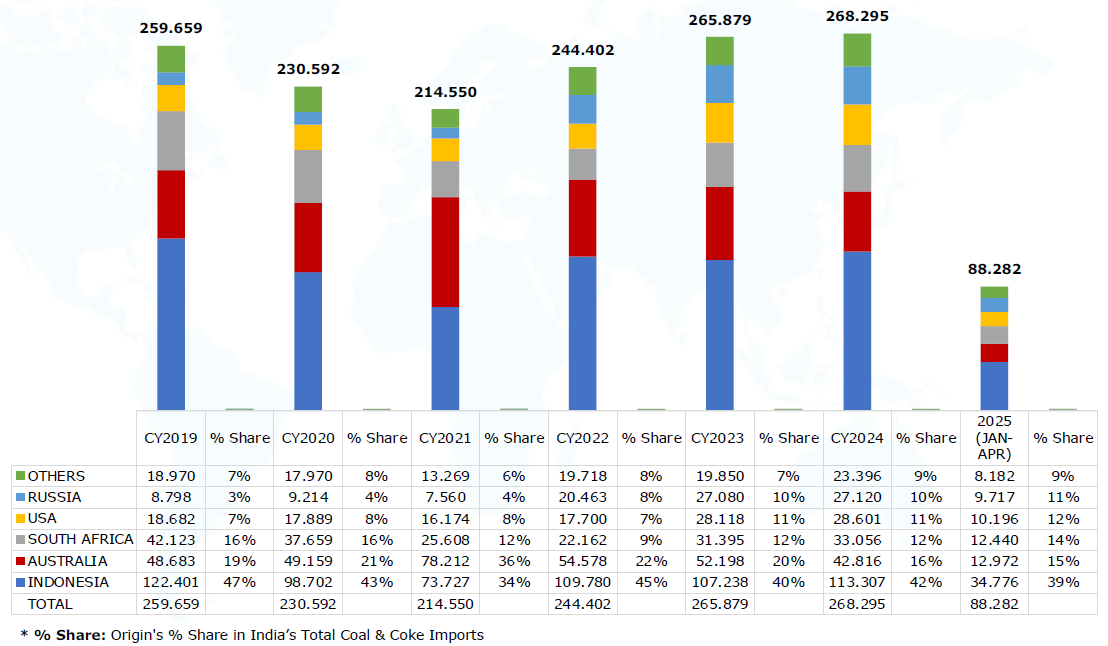

Supplier: Distribution of India's Coal and Coke Import Sources

It elaborates on India's coal and coke imports by origin, including its steam coal imports, coking coal imports, PCI coal imports, metallurgical coke imports, petroleum coke imports, and anthracite imports.

Buyer: Coal Imports by Industry

India's Coal and Coke Imports by Industry (1 million mt)

Discharge Point: Coal Imports by Port

It analyzes the data by combining India's coal and coke imports at various ports with import data from West Coast ports.

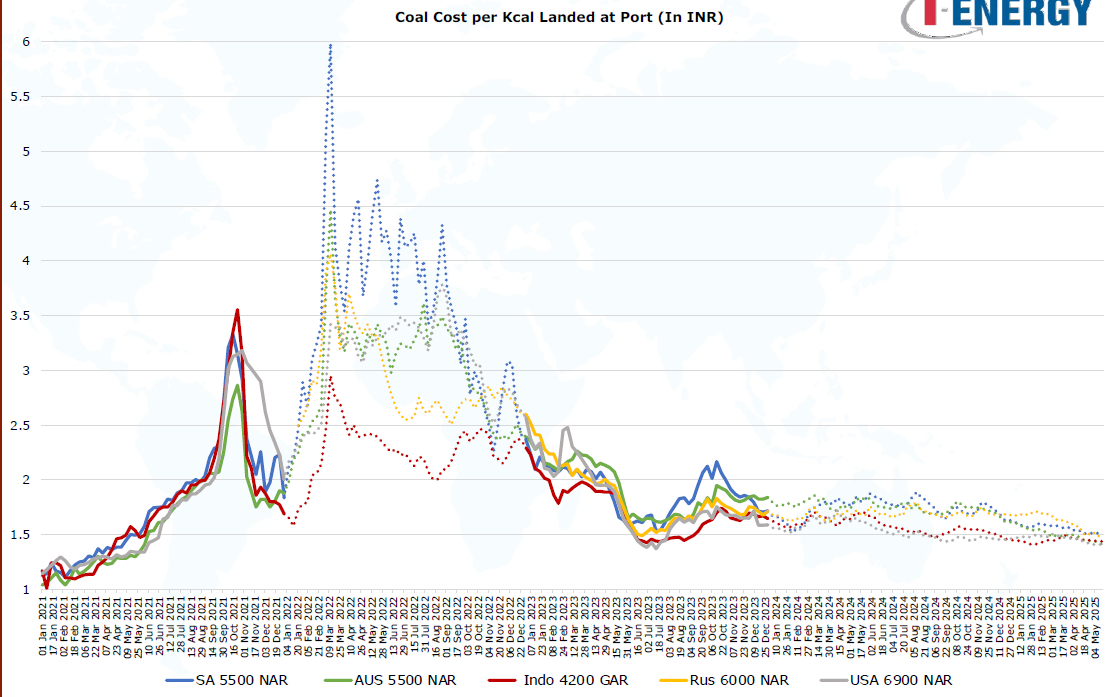

05 Cost Trend Tracking

Cost Trend Tracking: Unit Heat Value Cost of CIF Coal at Indian Ports

06 Future Outlook

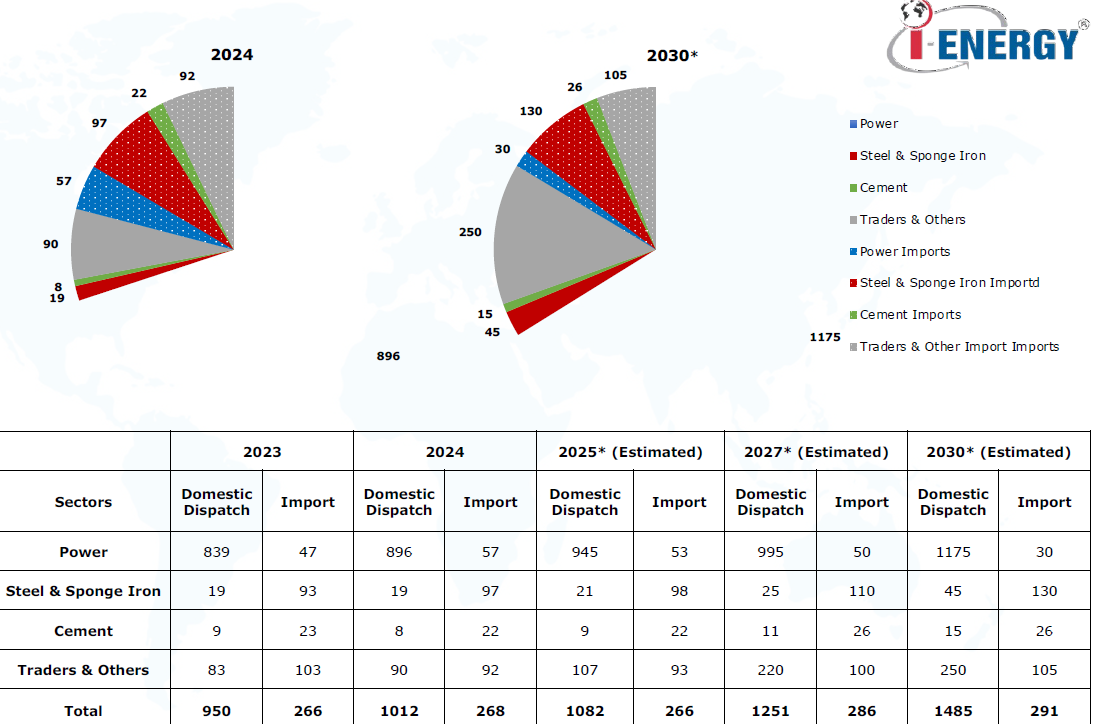

Future Outlook: Prospects for India's Coal Production and Imports

Projections

• India's imports are expected to reach a saturation point by 2030.

• Affected by the current market downturn, India's imports are projected to decline slightly by 2% YoY in 2025.

• India's domestic coal allocation to the power sector is expected to grow at a compound annual growth rate (CAGR) of approximately 4.6% until 2030.

• After 2027, allocations to non-power sectors will increase.

• Imports by the cement sector include steam coal and petroleum coke. Similar to this year, the cement sector is expected to prioritize petroleum coke over steam coal next year due to price advantages.

• The steel sector is expected to receive increased attention.

• Despite increased allocations to the steel sector, imports will continue to grow after 2030.

• A significant increase in commercial mining production will supplement supplies for traders and other industries.

• Imports of medium-to-low calorific value (CV) coal are expected to gradually decline, offset by domestic supply in India. Imports will be limited to industries requiring specific qualities or high-CV coal.

》Click to view the special report on the 2025 Indonesia Mining Conference & Critical Metals Conference